Finance Strategists is a leading financial education organization that connects people with financial professionals, priding itself on providing accurate and reliable financial information to millions of readers each year. The material quantity variance is also known as the material usage variance and the material yield variance. Of course, variances can be caused by production snafus, such as an excessive amount of scrap while setting up a production run, or perhaps damage caused by mishandling.

Formula

The first step in the calculation is to figure out how much stuffing material should be used to manufacture 9000 teddy bears (standard quantity). During a period, the Teddy Bear Company used 15,000 kilograms of stuffing material to produce 9000 teddy bears. Using the materials-related information given below, calculate the material variances for XYZ company for the month of October. Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise. This team of experts helps Finance Strategists maintain the highest level of accuracy and professionalism possible.

Sign up for the Dummies Beta Program to try Dummies’ newest way to learn.

The normal wastage and inefficiencies are taken into account while setting direct materials price and quantity standards. Variances are calculated and reported at regular intervals to ensure the quick remedial actions against any unfavorable occurrence. In this case, the production department performed efficiently and saved 40 units of direct material. Multiplying this by the standard price per unit yields a favorable direct material quantity variance of $160. As businesses strive for greater precision in cost management, advanced techniques in variance analysis have become increasingly valuable. One such technique is the use of trend analysis, which involves examining variance data over multiple periods to identify patterns and trends.

Question 3

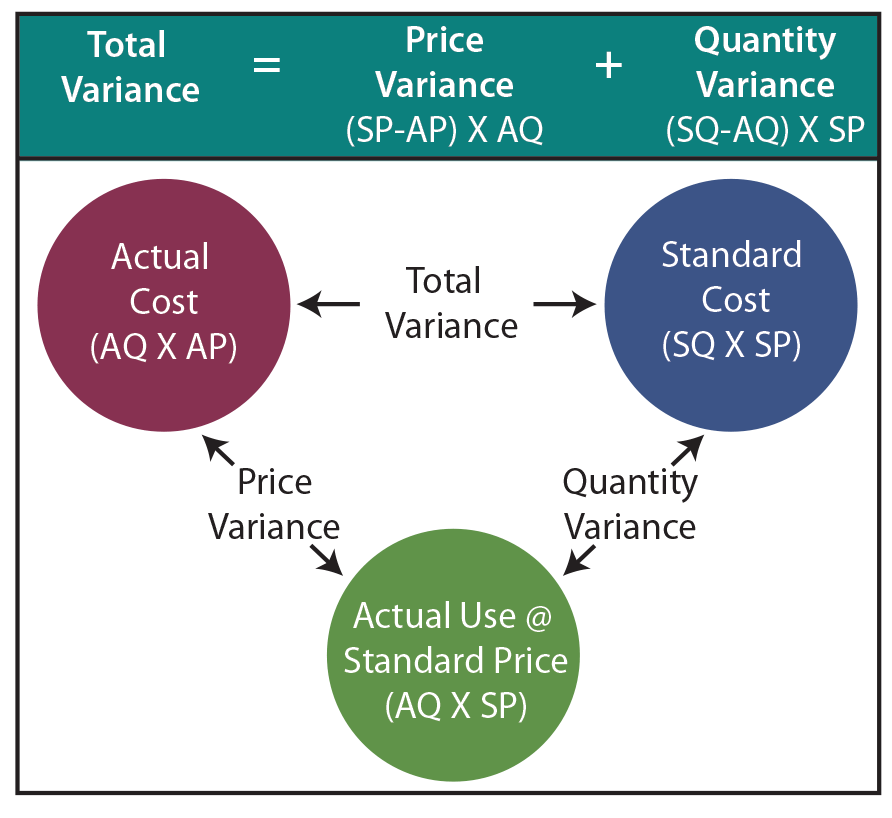

The first step in this analysis is to regularly review variance reports, which provide a snapshot of how actual costs compare to standard costs. These reports should be detailed and timely, allowing managers to quickly identify and address any discrepancies. The difference between the standard cost of direct materials and the actual cost of direct materials that an organization uses for production is known as Material Variance. So let’s say that you were producing a good and had set standard costs for labor at $100 per good and the standard cost for materials at $200 per unit.

- He has been the CFO or controller of both small and medium sized companies and has run small businesses of his own.

- The difference between the standard cost of direct materials specified for production and the actual cost of direct materials used in production is known as Direct Material Cost Variance.

- Armed with this knowledge, companies can focus their efforts on improving supplier lead times to achieve better cost control.

- Someone on our team will connect you with a financial professional in our network holding the correct designation and expertise.

- Thus, Variance Analysis is an important tool to keep a tab on the deviations from the standard set by a company.

The difference between the expected and actual cost incurred on purchasing direct materials, expressed as a positive or negative value, evaluated in terms of currency. The material quantity variance is a subset of the quantity variance, since it only applies to materials (or, more accurately, direct materials) that are used in the production process. Reliable suppliers who consistently deliver quality materials at agreed-upon prices help maintain stable production costs. Conversely, issues such as late deliveries, substandard materials, or unexpected price hikes can lead to variances. Building strong relationships with suppliers and regularly evaluating their performance can help businesses anticipate and address potential problems before they impact production. Together with the price variance the quantity variance forms part of the total direct materials variance.

If you’re looking for the PPV per unit, divide the total PPV by the number of units purchased by your business. To determine the total PPV for a specific order, subtract the standard amount from the actual amount. If feasible, at the end of every reporting period an analysis of purchase and production costs for capitalizability should be performed. You can calculate the standard quantity of materials by multiplying the standard quantity of materials per unit of output by the actual units of output produced in a given period.

This cross-functional collaboration ensures that all aspects of the business are aligned towards achieving cost efficiency. If there wasn’t enough supply available of the necessary raw materials, the company purchasing agent may have been forced to buy a more expensive alternative. If the company bought a smaller quantity of raw materials, they may not have qualified for favorable bulk pricing rates. In other words, if the business has consumed fewer materials to produce a given level of output than expected, the material quantity variance is said to be favorable. The material quantity variance in this example is favorable because the company manufactured the output using a lesser quantity of materials than what was planned in the budget. Direct materials quantity variance is also known as direct material usage or volume variance.

It also shows that the actual price per pound was $0.30 higher than standard cost (unfavorable). The direct materials used in production cost more than was anticipated, which is an unfavorable outcome. Direct material price variance (DM Price statement of retained earnings definition Variance) is defined as the difference between the expected and actual cost incurred on purchasing direct materials. It evaluates the extent to which the standard price has been over or under applied to different units of purchase.